2026–2028 Luxury Market Outlook (By Market Segment)

1. Trophy Estate Markets

(Bel Air / Holmby Hills, Beverly Hills, BHPO, Malibu, Malibu Beach, Sunset Plaza)

Profile: Global wealth enclaves, ultra-high pricing, but thin absorption.

- 2026:

- Absorption remains weak (20–30%).

- Inventory swells as discretionary sellers continue testing the market.

- Expect sporadic $50M–$100M trades, but overall volume subdued.

- 2027:

- Stabilization possible if global capital and interest rates ease.

- Median pricing edges up (+2–5%), but absorption lags.

- Market remains headline-driven rather than transactional.

- 2028:

- Recovery potential at the ultra-high end.

- Bel Air and Beverly Hills could reassert themselves with record-setting deals.

- Malibu bifurcates: prime oceanfront thrives, but inland properties move slowly.

Verdict: Glamour markets tied to global cycles. Eye-catching trophy sales, but shallow overall liquidity.

2. Core Westside Luxury

(Brentwood, Pacific Palisades, Santa Monica)

Profile: Lifestyle-driven, end-user heavy, balancing prestige and family appeal.

- 2026:

- Absorption holds at 40–50%.

- Median pricing plateaus (~flat to +3%).

- Still top choices for families seeking coastal quality of life.

- 2027:

- Demand strengthens as inventory balances.

- Median price growth accelerates (+5–8%).

- Strong school districts and lifestyle value maintain appeal.

- 2028:

- Expected to lead the broader luxury rebound.

- Absorption approaches 55–60%, comparable to pre-2020 levels.

Verdict: Emerging as the most reliable barometers of luxury market health.

3. Family Luxury Markets

(Encino, Sherman Oaks, Studio City, Valley Village, Cheviot Hills, Beverlywood)

Profile: High turnover, end-user dominated, strongest transactional base.

- 2026:

- Absorption 45–60% — far above trophy zones.

- Price growth steady (+2–4%).

- Driven by owner-occupiers rather than speculation.

- 2027:

- Volume leader across LA; consistent buyer pool sustains activity.

- Select neighborhoods (Cheviot Hills, Beverlywood) could see absorption near 65%.

- Values supported by relative affordability compared to the Westside.

- 2028:

- Likely to post record median prices, especially in Encino and Sherman Oaks.

- Families continue to migrate into these markets for larger homes and schools.

Verdict: The transaction engines of LA luxury — consistent liquidity, steady growth, and reliable demand.

4. Urban Lifestyle Markets

(West Hollywood, Hollywood Hills East)

Profile: Design-forward, entertainment-driven, younger buyer appeal.

- 2026:

- Absorption moderate (35–45%).

- Pricing holds steady, but renovation/design quality is decisive.

- 2027:

- West Hollywood stabilizes with lifestyle-driven buyers.

- Hollywood Hills East remains more erratic — some homes move quickly, others stagnate.

- 2028:

- Prices trend upward (+3–5%), though slower than Westside family markets.

- Remains attractive for investors and creatives but less consistent for end-users.

Verdict: Niche markets with steady but uneven absorption; style sells.

Macro Forecast (2026–2028)

- 2026: Flat-to-modest growth. Family markets outperform; trophy markets lag.

- 2027: Stabilization and early rebound, led by Core Westside and Family markets.

- 2028: Broad recovery. Transaction-heavy neighborhoods (Encino, Sherman Oaks, Beverlywood) and coastal lifestyle hubs (Brentwood, Palisades, Santa Monica) drive momentum. Trophy markets produce record sales but remain thin on volume.

Simplified Takeaway

- Transaction Engines: Encino, Sherman Oaks, Beverlywood, Cheviot Hills, Valley Village

- Market Benchmarks: Brentwood, Pacific Palisades, Santa Monica

- Trophy Headlines: Bel Air, Beverly Hills, BHPO, Malibu, Sunset Plaza

- Design Niches: West Hollywood, Hollywood Hills East

Macro Takeaways (2025)

-

Absorption Decline Across the Board

-

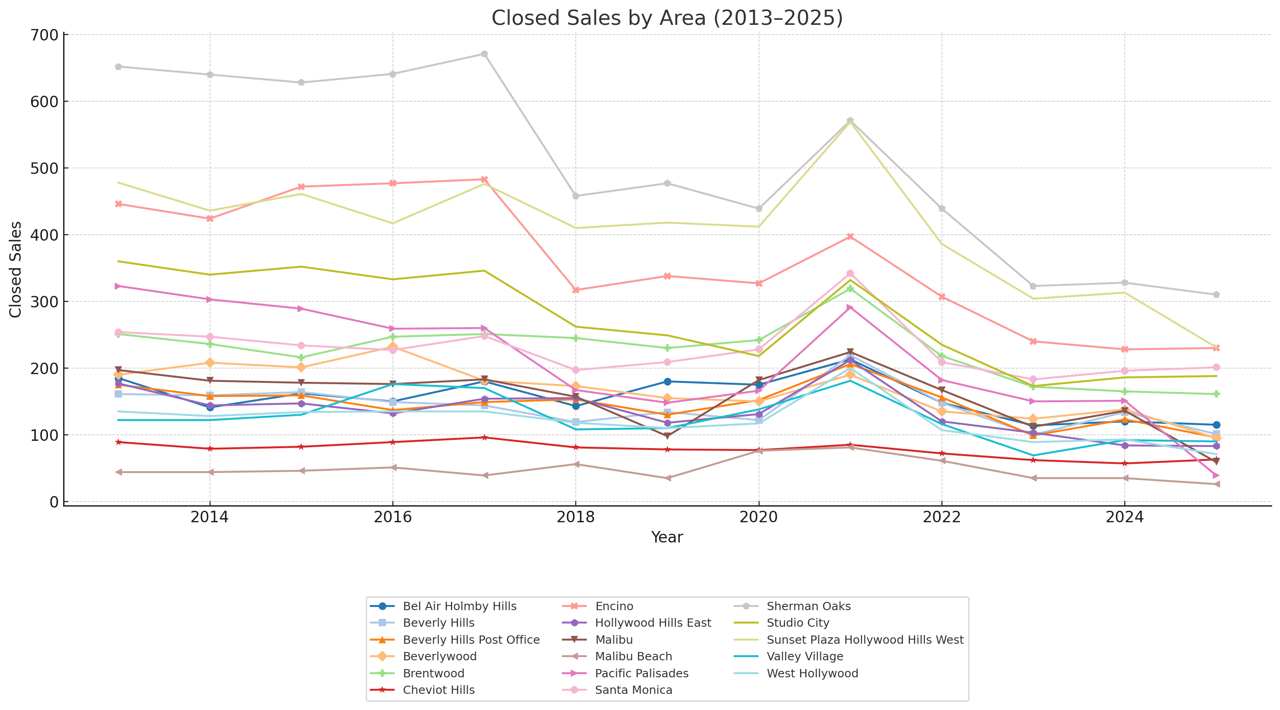

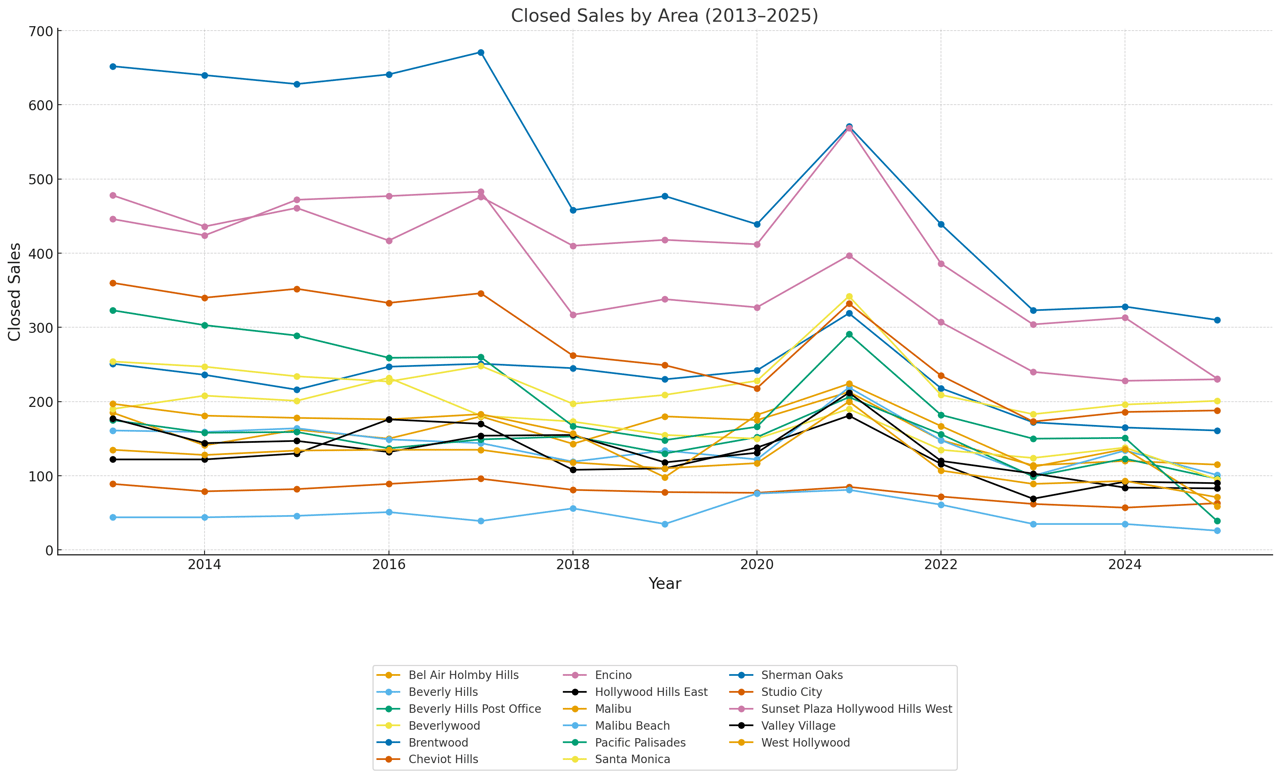

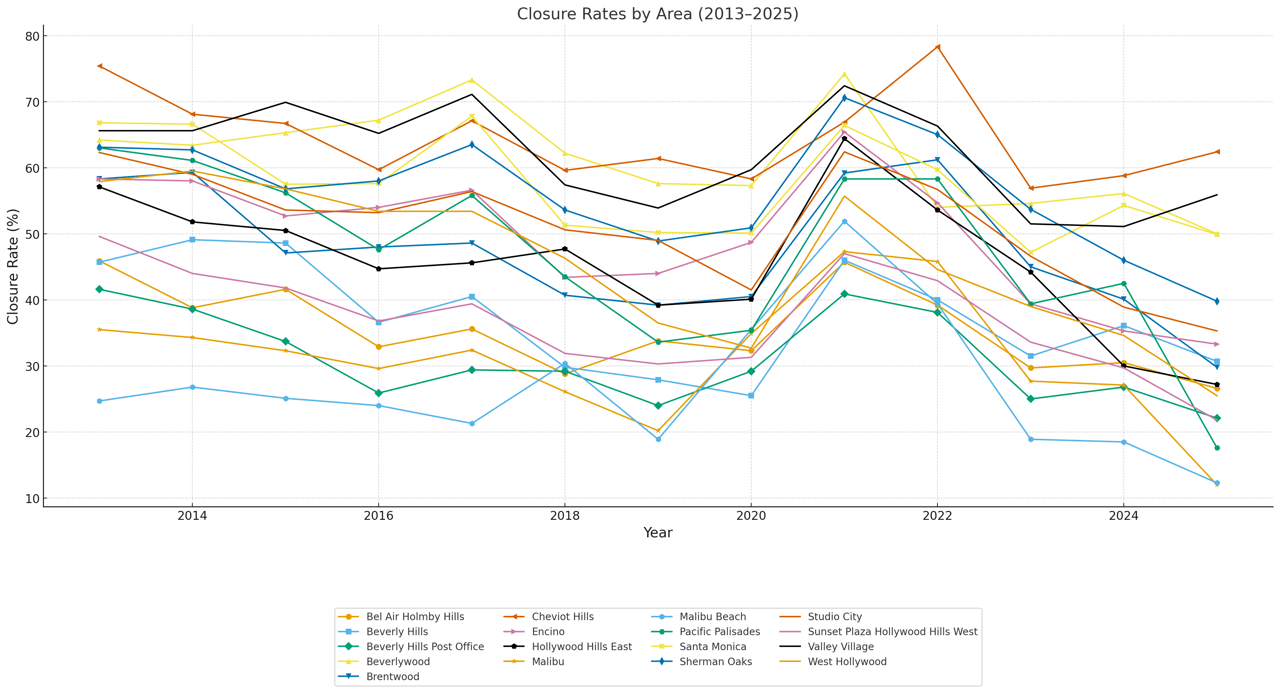

- Closure rates in 2025 are significantly lower than their historical averages in most luxury markets.

- Example:

- Bel Air/Holmby Hills dropped to 26.6% (vs. ~40% average historically).

- Beverly Hills Post Office at 22.1%, Malibu at 12%, Malibu Beach at 12.3%.

- Even stronger submarkets like Encino, Brentwood, and Pacific Palisades slipped into the 30% range.

➝ The data points to a cooling luxury market in 2025, with buyers absorbing far fewer listings compared to the surge of 2021.

-

Resilient Pockets Still Holding

- Despite the downturn, some neighborhoods maintained above-50% closure rates:

- Cheviot Hills: 62.4%

- Valley Village: 55.9%

- Beverlywood: 50%

- These areas are more end-user driven (family neighborhoods, mid-luxury price points), showing far less volatility than trophy-heavy zones.

➝ Owner-user demand neighborhoods are proving more stable, showing that the middle-luxury tier is more resilient than the ultra-luxury estate segment.

-

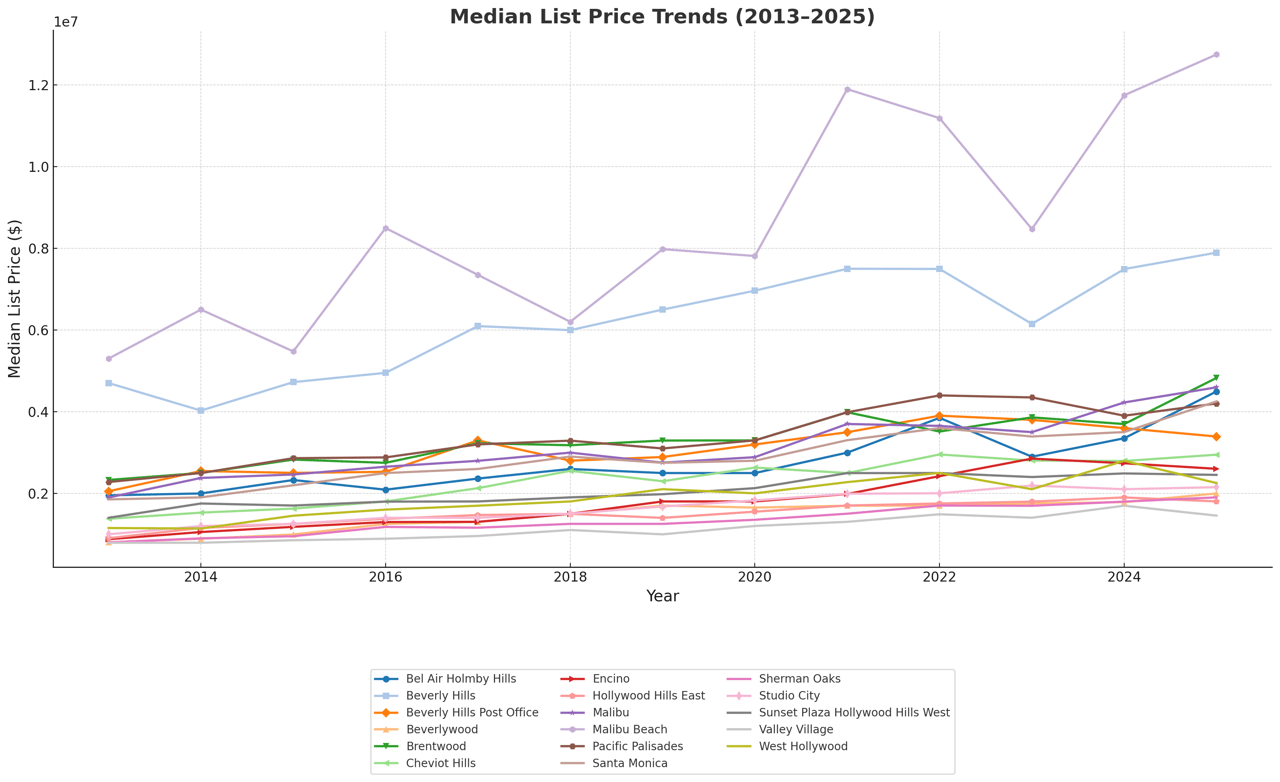

Price Trends in 2025

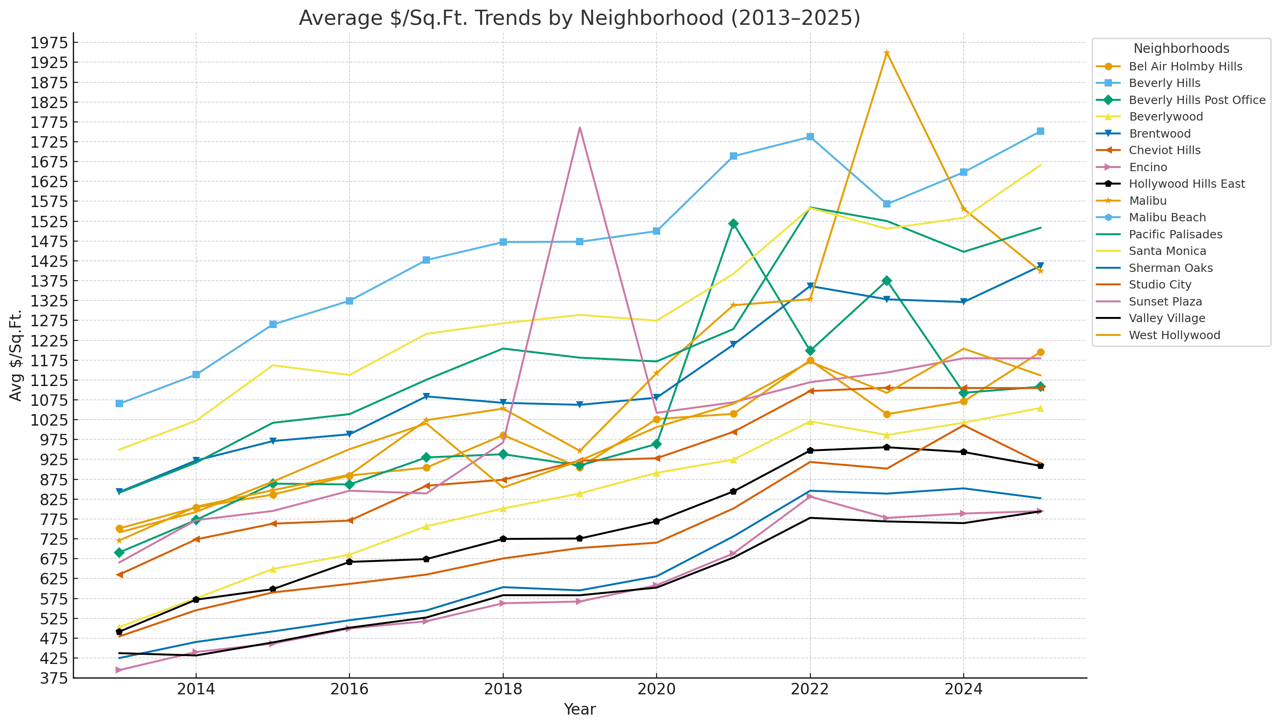

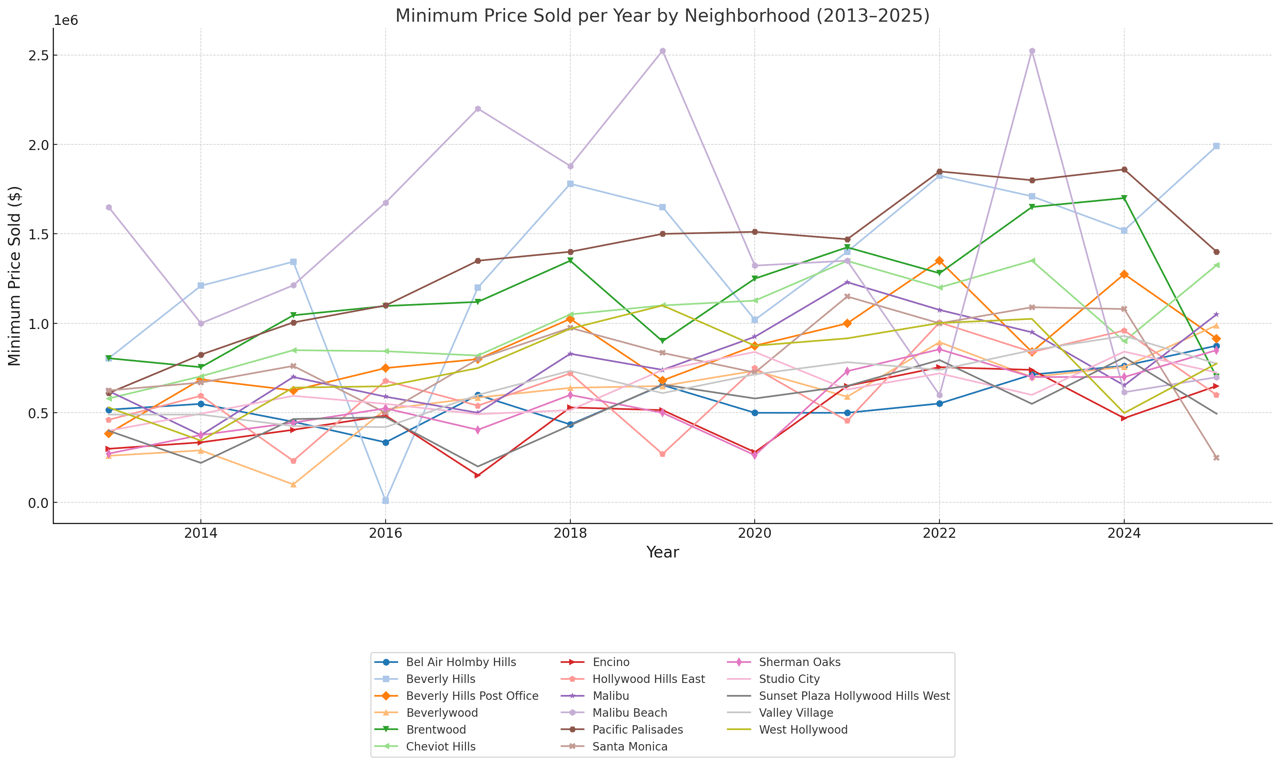

- Median Prices: Nearly all neighborhoods are at or near record highs despite lower absorption.

- Bel Air: ~$4.5M median.

- Beverly Hills: ~$7.9M median.

- Encino: ~$2.6M median.

- Malibu Beach: ~$12.7M median.

- Avg $/Sq.Ft. also peaked in many markets (Bel Air: $1,195/SF; Santa Monica: $1,666/SF; Malibu Beach: $3,343/SF).

➝ Sellers are holding price expectations, while buyers are slower to transact — classic luxury market standoff.

-

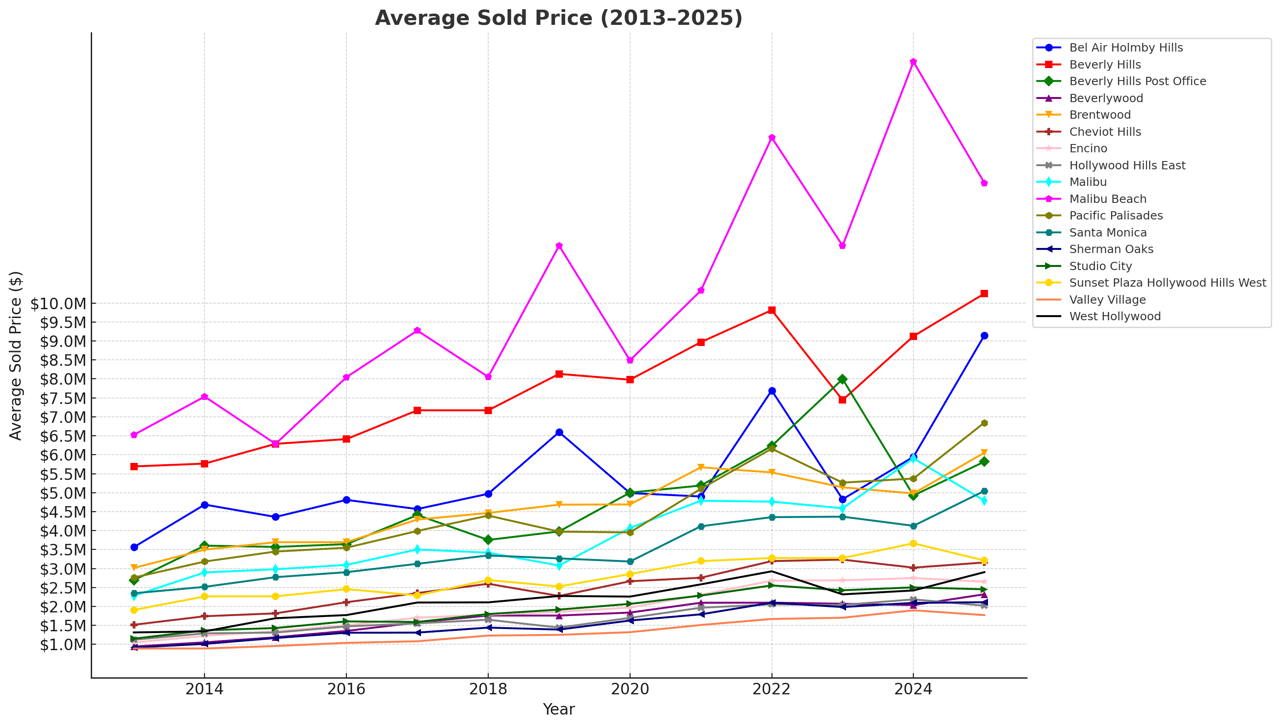

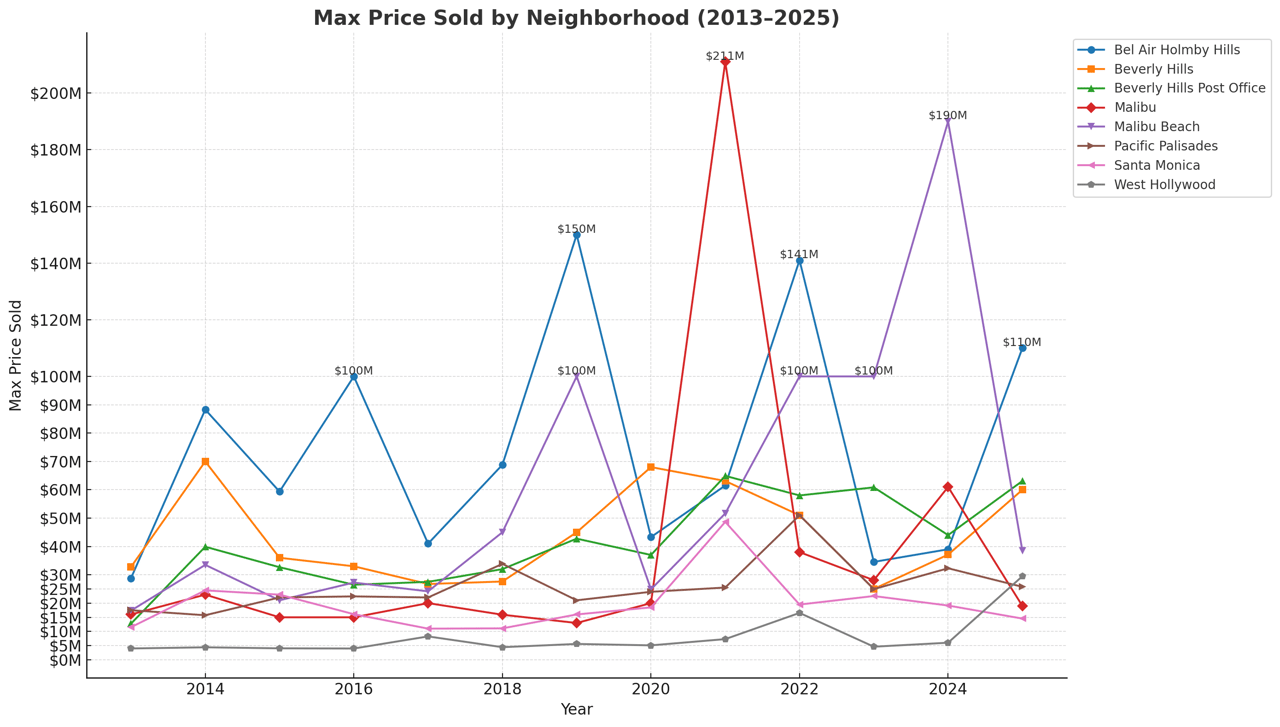

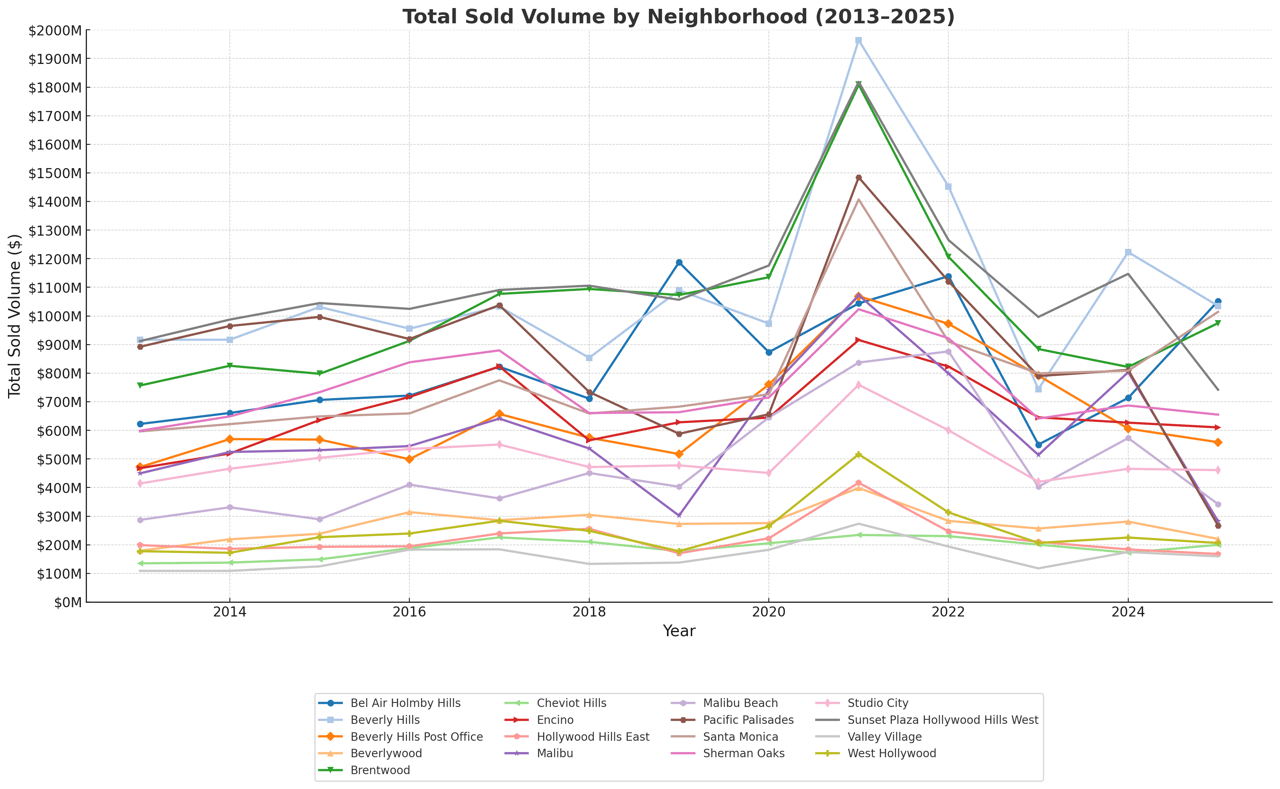

Volume Shrinkage

- Total sold volumes are down sharply in 2025 compared to the 2021 peak.

- Bel Air: ~$1.05B (down from $1.19B in 2019 but still strong).

- Beverly Hills: ~$1.03B (down ~50% from $1.96B in 2021).

- Malibu: ~$282M (down from over $1B in 2021).

- Santa Monica: ~$1.01B (still robust, showing strong stability).

➝ Fewer transactions but record-size deals still keep volumes inflated in trophy-driven areas.

-

Market Divide: Trophy vs. Family Neighborhoods

- Trophy Markets (Bel Air, BHPO, Malibu, Sunset Plaza): Weak absorption, huge spreads in pricing, reliant on global wealth cycles.

- Family Markets (Cheviot, Beverlywood, Sherman Oaks, Studio City, Valley Village): Higher absorption, less volatility, sustained demand from local buyers.

➝ The dataset underscores a two-tiered market: stable demand-driven neighborhoods vs. speculative/trophy-driven markets.

Overall 2025 Outlook

- Luxury slowdown: 2025 is a year of reduced velocity — fewer homes selling, longer times on market, and selective buyers.

- Seller resistance: Median prices remain high, showing sellers are unwilling to cut deeply, despite lower absorption.

- Safe havens: Mid-luxury, family-driven neighborhoods are the most stable investments, while trophy markets remain highly volatile but capable of record sales.

- Market signal: This looks like the tail end of a correction phase following the 2021–2022 peak frenzy, with the market trying to find equilibrium between seller expectations and buyer caution.

In plain terms:

2025 shows us a luxury market under pressure. Trophy neighborhoods are struggling to move product, while family-driven areas continue to trade at healthy rates. Prices are still high, but absorption is low, meaning buyers have more leverage, and the days of fast-paced bidding wars are behind us.

Most Resilient (Strong Absorption, Stable Growth)

These are neighborhoods where homes trade consistently year after year, with strong absorption, shorter DOM, and less reliance on a few extreme trophy sales.

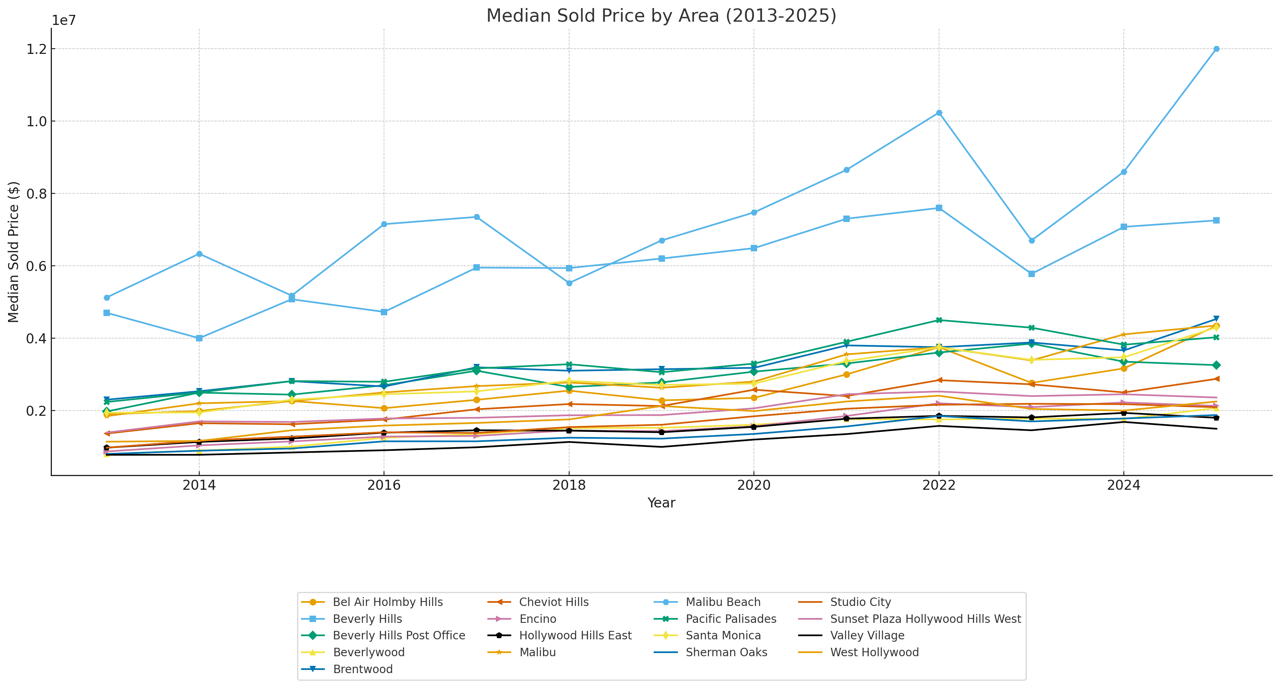

1. Beverlywood

- Absorption: Exceptionally high closure rates (often 60–74%) across 2013–2025.

- Median Prices: Steady climb from ~$800K in 2013 to ~$2M in 2025.

- Market Nature: A family-driven, middle-to-upper residential market. Consistent demand for entry-level luxury in central LA.

- Resilience Factor: Rare volatility, low trophy-dependence, extremely high sell-through ratio.

2. Cheviot Hills

- Absorption: Very high closure rates (60–78%) nearly every year.

- Median Prices: Steady increase from ~$1.3M in 2013 to ~$2.9M in 2025.

- Market Nature: Strong owner-user neighborhood with stable school-driven demand.

- Resilience Factor: Predictable appreciation and turnover.

3. Sherman Oaks / Studio City / Valley Village

- Absorption: Strong, with closure rates in the 50–70%+ range.

- Median Prices: Consistent upward growth, generally doubling since 2013.

- Market Nature: Valley submarkets with large buyer pools, diverse housing stock, and steady family demand.

- Resilience Factor: Bread-and-butter luxury, not trophy-reliant, with relatively balanced markets even in slower years.

Moderately Resilient (Prestige + Family Mix, Some Volatility)

These markets are strong but show more fluctuation when broader luxury sentiment shifts.

4. Brentwood

- Absorption: Solid, usually 40–60%, dipping in weaker years but bouncing back.

- Median Prices: Rose steadily from ~$2.3M in 2013 to ~$4.8M in 2025.

- Market Nature: Large neighborhood with a mix of $3M–$10M family homes and some higher-end estates.

- Resilience Factor: Broad buyer base softens volatility, but exposure to the $20M+ range introduces some swings.

5. Beverly Hills (Proper)

- Absorption: Volatile, closure rates from 25–49%, but volume is always high.

- Median Prices: Stable upward climb, ~$4.7M in 2013 → ~$7.9M in 2025.

- Market Nature: Global brand neighborhood with consistent demand, but tied to wealth cycles.

- Resilience Factor: Less steady than Brentwood, but anchored by brand cachet that maintains global demand.

6. Pacific Palisades

- Absorption: Moderate (30–60%), with some years dipping below 40%.

- Median Prices: ~$2.2M in 2013 → ~$4.2M in 2025.

- Market Nature: Large, family-driven luxury market with both middle-luxury and high-end bluffs/ocean estates.

- Resilience Factor: Generally stable, but performance varies based on Westside market cycles.

7. Encino

- Absorption: Strong in some years (60–65%) but dips to mid-30s in others.

- Median Prices: ~$874K in 2013 → ~$2.6M in 2025.

- Market Nature: Hotter since the rise of “modern spec mansions,” but reliant on trend-driven demand.

- Resilience Factor: Strong family demand, but trophy builds have made it more cyclical.

Most Volatile (Trophy-Driven, Low Liquidity, Global Buyer Dependent)

These neighborhoods swing based on ultra-high-net-worth activity, trophy estate sales, and market cycles.

8. Bel Air / Holmby Hills

- Absorption: Among the lowest, often 25–35%, despite huge dollar volume.

- Median Prices: ~$2M in 2013 → ~$4.5M in 2025, but wide swings in $50M–$150M trophy sales distort averages.

- Market Nature: Iconic trophy market with estates traded globally.

- Volatility Factor: Sales volume and absorption fluctuate heavily depending on billionaire activity.

9. Beverly Hills Post Office (BHPO)

- Absorption: Consistently low (22–40%).

- Median Prices: ~$2M in 2013 → ~$3.3M in 2025.

- Market Nature: A hybrid zone: more accessible than Beverly Hills proper, but less cachet.

- Volatility Factor: Vulnerable to slowdowns; not as resilient as Sherman Oaks or Beverlywood.

10. Malibu & Malibu Beach

- Absorption: Very low, often 12–35%.

- Median Prices: Spikes massively (e.g., Malibu Beach median from ~$5M in 2013 to ~$12.7M in 2025).

- Market Nature: Trophy-driven, reliant on ultra-high-net-worth buyers and vacation-home demand.

- Volatility Factor: Extremely volatile, with droughts in activity followed by bursts of record-breaking sales.

11. Sunset Plaza / Hollywood Hills West

- Absorption: Weak, often 20–40%, despite huge listing counts.

- Median Prices: ~$1.3M in 2013 → ~$2.4M in 2025, but wide swings in $20M–$70M deals.

- Market Nature: Spec-driven, international buyer appeal, heavy in modern estates.

- Volatility Factor: Spec mansion market makes it especially cyclical.

12. West Hollywood

- Absorption: Middling (25–55%), declining in later years.

- Median Prices: ~$1.1M in 2013 → ~$2.25M in 2025.

- Market Nature: More condo/mixed inventory than true estate market.

- Volatility Factor: Relies on condo turnover and developer projects, weaker resilience than valley single-family.

Takeaway

- Stable “workhorse” markets: Cheviot Hills, Beverlywood, Santa Monica, Sherman Oaks, Studio City, Valley Village.

- Cyclical prestige markets: Brentwood, Pacific Palisades, Encino, Hollywood Hills East, West Hollywood.

- Volatile trophy enclaves: Sunset Plaza, BHPO, Bel Air, Malibu, Malibu Beach.

Download Market Report