17,372 people live in Malibu Beach, where the median age is 49 and the average individual income is $117,637. Data provided by the U.S. Census Bureau.

Total Population

Median Age

Population Density Population Density This is the number of people per square mile in a neighborhood.

Average individual Income

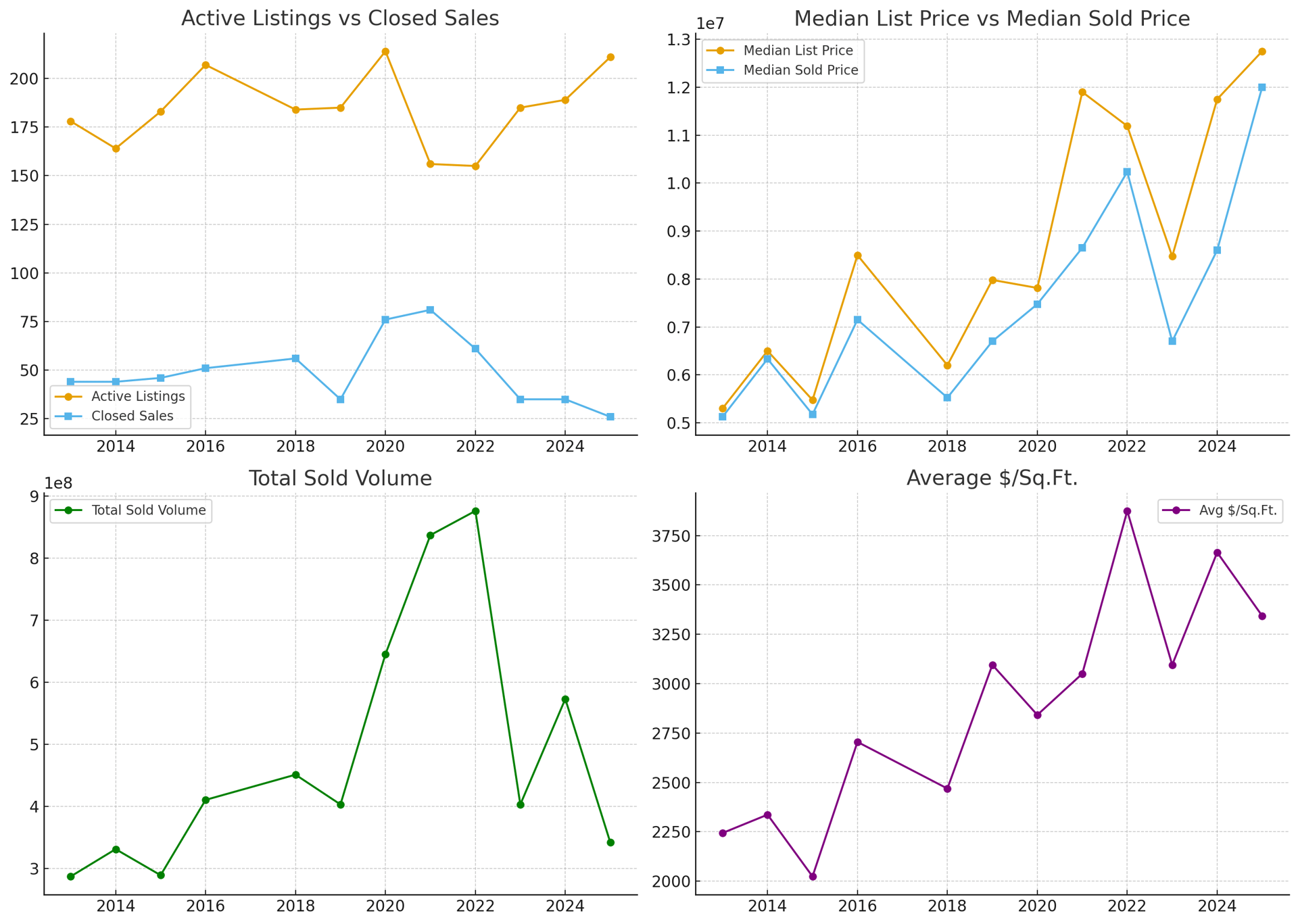

1. Active Listings & Closed Sales

Projection:

2. Closure Rate (Absorption)

3. Pricing Trends

4. Total Sold Volume

Projection:

5. Value Per Square Foot

6. Sale-to-List Ratios

Bottom Line

Malibu Beach is entering a low-volume, high-price equilibrium:

1. Market Activity: Active Listings & Closed Sales

2. Closure Rate (Absorption)

3. Pricing Trends: Median List vs. Median Sold

4. Total Sold Volume

5. Value Per Square Foot

6. Sale-to-List Ratios

What This Means

Bottom Line

Malibu Beach has shifted from ultra-hot luxury liquidity (2021–22) to a thin, illiquid market (2023–25). Trophy homes can still fetch record $/Sq.Ft., but broader absorption is extremely weak.

Malibu Beach has 6,119 households, with an average household size of 2. Data provided by the U.S. Census Bureau. Here’s what the people living in Malibu Beach do for work — and how long it takes them to get there. Data provided by the U.S. Census Bureau. 17,372 people call Malibu Beach home. The population density is 707 and the largest age group is Data provided by the U.S. Census Bureau.

Total Population

Population Density Population Density This is the number of people per square mile in a neighborhood.

Median Age

Men vs Women

Population by Age Group

0-9 Years

10-17 Years

18-24 Years

25-64 Years

65-74 Years

75+ Years

Education Level

Total Households

Average Household Size

Average individual Income

Households with Children

With Children:

Without Children:

Marital Status

Blue vs White Collar Workers

Blue Collar:

White Collar:

There's plenty to do around Malibu Beach, including shopping, dining, nightlife, parks, and more. Data provided by Walk Score and Yelp.

Explore popular things to do in the area, including Rancho Escondido, Nesse Foods, and Malibu Organic Lemon Company.

| Name | Category | Distance | Reviews |

Ratings by

Yelp

|

|---|---|---|---|---|

| Dining · $ | 0.75 miles | 0 reviews | 0/5 stars | |

| Dining | 0.75 miles | 0 reviews | 0/5 stars | |

| Dining | 0.75 miles | 0 reviews | 0/5 stars | |

| Dining | 0.75 miles | 0 reviews | 0/5 stars | |

| Dining · $$ | 0.75 miles | 0 reviews | 0/5 stars | |

| Active | 0.75 miles | 0 reviews | 0/5 stars | |

| Active | 0.75 miles | 0 reviews | 0/5 stars | |

| Active | 0.75 miles | 1 review | 5/5 stars | |

| Active | 0.75 miles | 6 reviews | 4.5/5 stars | |

| Active | 0.75 miles | 0 reviews | 0/5 stars | |

| Active | 0.75 miles | 6 reviews | 5/5 stars | |

| Active | 0.75 miles | 31 reviews | 4.2/5 stars | |

| Active | 0.75 miles | 2 reviews | 5/5 stars | |

| Active | 0.75 miles | 3 reviews | 5/5 stars | |

| Active | 0.75 miles | 28 reviews | 5/5 stars | |

| Nightlife | 0.75 miles | 0 reviews | 0/5 stars | |

| Beauty | 0.75 miles | 3 reviews | 5/5 stars | |

| Beauty | 0.75 miles | 0 reviews | 0/5 stars | |

| Beauty | 0.75 miles | 0 reviews | 0/5 stars | |

| Beauty | 0.75 miles | 19 reviews | 4.8/5 stars | |

| Beauty | 0.75 miles | 0 reviews | 0/5 stars | |

| Beauty | 0.75 miles | 3 reviews | 5/5 stars | |

| Beauty | 0.75 miles | 0 reviews | 0/5 stars | |

| Beauty | 0.75 miles | 0 reviews | 0/5 stars | |

|

|

||||

|

|

||||

|

|

||||

|

|

||||

|

|

||||

|

|

Service Agreement.

We Will Run a Custom Search or Marketing Plan for Your specific needs.